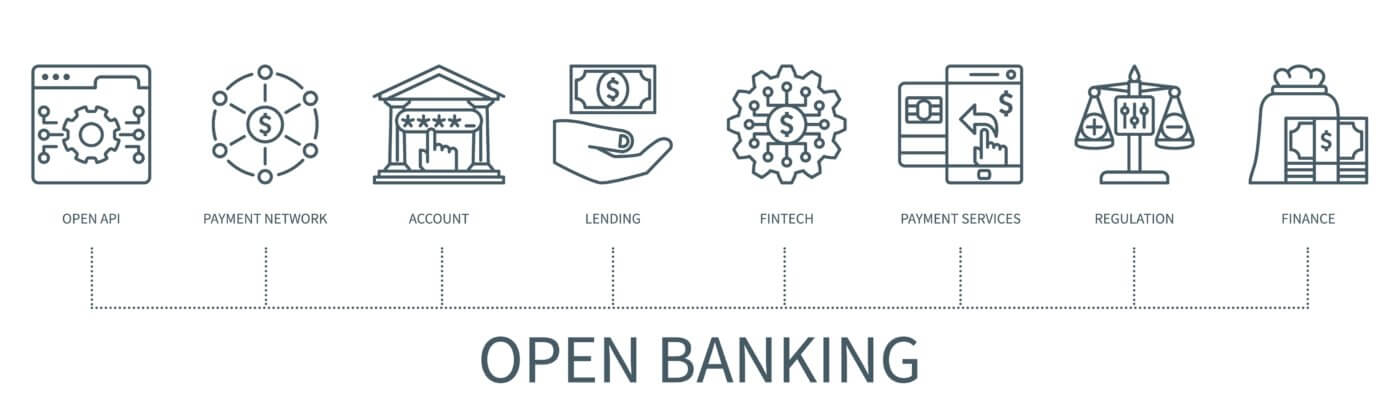

The State of Open Banking

As we enter the next decade, Open Banking will accelerate from the regulatory to the implementation stages in North America. Look no further than Europe for positive clues of the impact on consumer banking with now more than 63 million Open Banking users led by the UK, followed by Germany, Sweden, and the Netherlands. The EU continues to evolve its program with the introduction of its PSD3 program in 2026, further elevating and standardizing practices. The US timeframe follows that of the EU with the Consumer Financial Protection Bureau under Section 1033 of the Dodd-Frank Act, which will allow by 2026 consumers greater control over their financial data. The big difference between the EU is the premise that the U.S. model is industry versus government-led, enabling market forces to help shape the standards. Canada is also following suit as part of a multi-phase approach with full deployment in 2025 and combines the best of the EU and US frameworks.

Open banking will significantly impact how institutions provide services and retain customer loyalty. The platform will usher in a truly seamless banking experience by allowing streamlined access to multiple financial services from different providers through a single platform. With the average customer holding two or more financial accounts, some of which are provided by fintech companies, this more efficient and user-friendly experience will accelerate the decline of branch visits for transactional reasons. However, not all is lost for financial institutions that are well-positioned to leverage the wealth of customer data they capture by converting these into personalized services and products, adding a new layer of stickiness to their primary institution. Open Banking will also continue to accelerate the collaboration between fintech and financial institutions, offering new services not previously available due to scale or cost. Mobile will become the hub as it continues to dominate as the primary channel for transactional banking and Open Banking will continue to shift usage to this platform, providing greater convenience in the palm of the customer’s hand.

Image Source: Shutterstock

Three Opportunities to Leverage the Brand Network

With many institutions revisiting their branch network towards smaller, more efficient experiences, we have identified three major opportunities to leverage the impact of Open Banking around an intertwined triad of human, physical, and digital experiences, namely:

1. Opportunity: Shift From Transactional to Advisory Focus:

Our study on the greater opportunity for financial institutions to lead in becoming the customer’s trusted financial advisor during and further to the launch of Open Banking will be paramount. With the decline of branch transactional visits, filling the void with only 5 percent of customers view their institutions as a place for trusted financial advice. The branch design must incorporate a higher level of tiered privacy, allowing staff to comfortably engage with customers in an intimate environment. Future-proofing the branch experience will be top of mind as the migration away from transactions will take a decade or so to fully materialize.

Converting the conventional teller line through a series of phases, from stand-up to sit-down, from linear to modular will be critical in anticipating and adjusting the customer and staff sales choreography. The acceleration of digital queuing system adoption and its integration with new lobby leader roles will help manage the transition while also reducing customer banking frustrations. The introduction of virtual meeting rooms enabling greater access to experts will continue to evolve, creating holodeck-type experiences we first highlighted in our work with Intel five years ago.

2. Integration of Digital Tools in Branches:

Branches have already started the shift of untethering the teller platforms and allowing staff to move the conversation seamlessly into private rooms. This is just the beginning as new digitally assisted sales platforms will usher in mobile-inspired digital tools that utilize open banking data to provide real-time insights into customer accounts and preferences. This integration can enhance the in-branch experience by enabling staff to offer more relevant advice and solutions based on comprehensive customer profiles.

Digital signing will also continue to evolve and play a greater role in customizing the message pending the community customer profiles and dayparting based on what is the most relevant message. We will also witness the seamless integration of digital signing and mobile devices. Geo-located messaging, a promise for the past decade will also become a reality as customers have greater confidence in the security of their data.

Image Source: Shutterstock

3. New Branch Staffing Model and Sales Choreography:

We will witness a shift in who and why we hire customer-facing talent and the role they play in driving growth. In-branch processes focused on efficiencies will reach their maturity and the shift will focus on curated personal advice-driven engagements. AI will assist in ensuring the staff reflects the right level of empathy in addition to humanistic skills to build trust and confidence in the advice being provided. Although we will witness a flattening of the branch staffing level currently underway, the roles and responsibilities these individuals provide will be significantly different than today’s model.

Staffing experience and capabilities will also be customized to the given location of the branch as witnessed by many of the European banks such as Millennials BCP Bank which established a series of banking ecosystems tailored to the given customer community segments. The days of offering the same services irrespective of branch size will shift with Open Banking towards clustering of products and offerings delivered by experts pending the location and customer make-up.

In summary, open banking is set to redefine the branch experience by making banking more accessible, personalized, and competitive. As banks adapt to these changes, they will likely focus on enhancing customer relationships and providing value-added services through better employee engagement, seamless digital channels, and advice-centric physical locations.

On a Final Note

Open banking is set to redefine the branch experience by making banking more accessible, personalized, and competitive. As banks adapt to these changes, they will likely focus on enhancing customer relationships and providing value-added services through better employee engagement, seamless digital channels, and advice-centric physical locations.

{kind=link}

{kind=link}